Categories

NewsPublished November 21, 2025

53% of U.S. Homes Lost Value: What This Historic Decline Means for Everett and Bothell

53% of U.S. Homes Lost Value: What This Historic Decline Means for Everett and Bothell

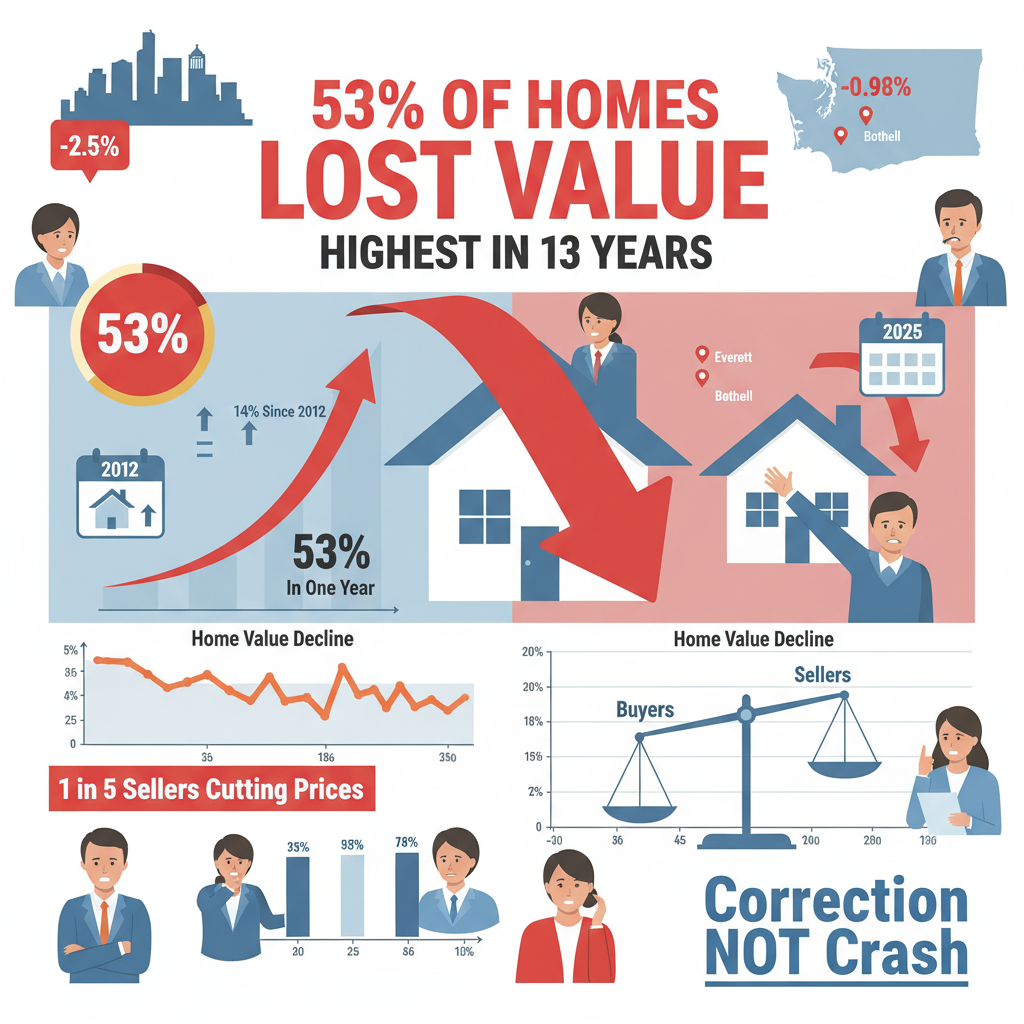

Breaking News - November 21, 2025: 53% of U.S. homes have lost value over the past year—the highest share of depreciation in 13 years since 2012. This share has climbed from just 14% a year ago, marking a dramatic shift in the housing market. Meanwhile, Seattle home prices dropped 2.5% in September, and Washington state saw prices decline 0.98% year-over-year. What does this historic depreciation mean for Everett and Bothell homeowners and buyers?

As a Realtor with Keller Williams Everett, I'm helping clients navigate this unprecedented market shift. Let's break down what's happening nationally and locally, and show you how to make smart decisions in this changing landscape.

The Numbers: Historic Home Value Decline

October 2025 data reveals the most widespread depreciation since 2012.

National data:

- 53% of homes lost value over past year

- Highest depreciation share in 13 years

- Climbed from just 14% one year ago

- Based on Zillow Zestimate data

- Most widespread decline since Great Recession recovery

Pacific Northwest data:

- Seattle prices down 2.5% (September 2025)

- Washington state down 0.98% year-over-year

- Seattle-Tacoma-Everett region experiencing price drops

- Nearly 1 in 5 Seattle sellers cutting prices

- Inventory growing while demand softens

What this means: We're experiencing the most significant value correction since the post-recession period.

Why Are Home Values Declining?

Multiple factors converged to create this depreciation wave.

1. Mortgage Rates Remain Elevated

Despite recent dips, rates still deterring buyers.

Rate reality:

- Hovering around 6.5% (down from 7%+ but still high)

- Experts agree: 2-3% rates won't return in our lifetimes

- Monthly payments significantly higher than 2020-2021

- Affordability stretched for most buyers

- Rate sensitivity keeping buyers cautious

The impact: High rates suppress demand, putting downward pressure on prices.

2. The Lock-In Effect Constrains Supply

Homeowners with low rates won't sell.

The problem:

- Seattle home-sale turnover plunged to 2% (from 3.2% in 2019)

- Homeowners with 3-4% rates trapped

- Trading up means doubling mortgage rate

- Monthly payment shock prevents moves

- Market feels "frozen in place"

The paradox: Inventory growing but not from existing homeowners—they're staying put.

3. Affordability Crisis Persists

Prices still near historic highs despite declines.

Affordability challenges:

- Median Seattle price still around $854,000

- Down payment requirements substantial

- Income-to-price ratios challenging

- Student debt and obligations limiting capacity

- First-time buyers priced out

The reality: Small price drops don't solve fundamental affordability issues.

4. Economic Uncertainty

Broader concerns keeping buyers cautious.

Uncertainty factors:

- Builder sentiment weakening

- Job market showing softness

- Buyer hesitation widespread

- Stock market volatility

- Recession fears persisting

The hesitation: Buyers waiting for stability that may not come.

What This Means for Everett and Bothell

National trends play out with local characteristics.

Everett's Value Trajectory

Everett experiencing price adjustments but maintaining stability.

Everett dynamics:

- Part of Seattle-Tacoma-Everett region seeing declines

- Lower price points ($500k-$700k) more resilient

- Boeing workforce stability supporting baseline demand

- Downtown revitalization creating long-term value

- Waterfront properties seeing larger adjustments

The reality: Everett values declining but less dramatically than premium Seattle neighborhoods.

Bothell's Premium Market Adjustment

Bothell's higher-end market experiencing correction.

Bothell trends:

- Premium homes ($800k+) seeing price cuts

- Nearly 1 in 5 sellers reducing prices

- Excellent schools maintaining floor on values

- Tech sector recovery supporting demand

- New construction competing with resale

The opportunity: Bothell's quality-of-life premium now more accessible.

Snohomish County Market Reality

Our county positioned between extremes.

Local advantages:

- More affordable than King County

- Less dramatic declines than Seattle proper

- Strong employment base supporting values

- Population growth continuing

- Infrastructure improvements ongoing

The positioning: Snohomish County experiencing modest declines, not collapse.

Is This a Housing Market Crash?

No—this is a correction, not a collapse.

Why This Isn't 2008

Key differences from Great Recession.

Critical distinctions:

- No subprime lending crisis

- Homeowners have substantial equity

- Lending standards remain strict

- No foreclosure wave

- Inventory growing gradually, not flooding

The reality: This is a normalization, not a crisis.

Why Values Are Declining

Natural market correction after unprecedented run-up.

The context:

- Home prices rose 60% from 2019-2023

- Correction brings prices closer to fundamentals

- Affordability improving (slowly)

- Market finding sustainable equilibrium

- Healthy adjustment, not panic

The perspective: 53% losing value sounds scary, but many still have significant gains from pandemic era.

What "Lost Value" Really Means

Understanding the numbers in context.

The reality:

- Most "losses" are 1-5%, not dramatic drops

- Many homeowners still have equity from pandemic gains

- Seattle down 2.5% but up 40%+ since 2019

- Washington down 0.98% year-over-year

- Modest correction, not catastrophic decline

The truth: If you bought in 2020-2021, you're likely still ahead.

How Buyers Should Respond

This depreciation creates opportunities for strategic buyers.

Strategy 1: Recognize This as Your Window

Values declining means better entry points.

The opportunity:

- Prices more reasonable than 6 months ago

- Seller desperation increasing

- Negotiating power at decade high

- Less competition from other buyers

- Time to be selective

The reality: This is the buyer's market you've been waiting for.

Strategy 2: Don't Wait for the Bottom

Timing the exact bottom is impossible.

Why act now:

- Rates could rise again

- Inventory could get absorbed

- Spring market may bring competition

- Good homes still sell quickly

- Perfect timing doesn't exist

The wisdom: Buy when you find the right home at fair price, not when market hits theoretical bottom.

Strategy 3: Negotiate Aggressively

Declining values give you leverage.

Negotiation tactics:

- Offer below asking on overpriced homes

- Point to recent comparable sales showing declines

- Request seller-paid closing costs

- Demand repairs or credits

- Use days-on-market as leverage

The advantage: Sellers know values are declining—use that knowledge.

Strategy 4: Focus on Long-Term Value

Short-term fluctuations matter less than fundamentals.

What to prioritize:

- Location, location, location

- School districts and amenities

- Neighborhood trajectory

- Property condition and bones

- Your lifestyle needs

The perspective: Buy for 7-10 years, not 1-2 years.

Strategy 5: Get Pre-Approved and Ready

Opportunity favors the prepared.

Action steps:

- Full mortgage pre-approval

- Down payment funds liquid

- All documentation ready

- Credit optimized

- Ready to move quickly on right property

The advantage: When right home appears, you can act immediately.

How Sellers Should Respond

Declining values require strategic adjustments.

Accept the New Reality

Values are declining—denial won't help.

The reality:

- 53% of homes losing value nationally

- Seattle down 2.5%, Washington down 0.98%

- Nearly 1 in 5 Seattle sellers cutting prices

- Buyers have leverage

- Market has fundamentally shifted

The choice: Adapt pricing or watch your home sit.

Price Aggressively from Day One

In declining market, pricing is everything.

Pricing strategy:

- Price BELOW recent comparable sales

- Account for declining trend

- Attract buyers immediately

- Avoid multiple price cuts

- Get appraisal-ready from start

The reality: Homes priced right still sell—overpriced ones languish.

Make Your Home Irresistible

Competition for buyers is fierce.

How to compete:

- Professional staging and photography

- Complete all repairs before listing

- Deep clean and declutter

- Enhance curb appeal

- Offer buyer incentives

The advantage: Presentation matters MORE in declining market.

Be Flexible and Realistic

Rigid sellers fail in this environment.

Flexibility wins:

- Accommodate showing requests

- Negotiate repairs reasonably

- Consider creative terms

- Offer closing cost assistance

- Stay realistic about market

The reality: Flexible sellers close deals; inflexible ones sit and watch values decline further.

Consider Timing Carefully

Should you wait or sell now?

Factors to consider:

- Are values still declining in your area?

- Do you NEED to sell or just want to?

- Can you afford to wait 6-12 months?

- Will spring market be better?

- What's your financial situation?

The calculation: If you must sell, do it now. If you can wait, monitor market carefully.

What Homeowners Should Know

Already own? Here's what this means for you.

Don't Panic About Paper Losses

Unrealized losses only matter if you sell.

The perspective:

- If you're not selling, daily value fluctuations don't matter

- Long-term real estate appreciates

- You're building equity through mortgage paydown

- You have housing stability

- Short-term declines are normal

The wisdom: Real estate is long-term investment, not day-trading.

Understand Your Equity Position

Context matters for your specific situation.

Questions to ask:

- When did you buy?

- What's your mortgage balance?

- How much equity do you have?

- Are you underwater or still ahead?

- What's your long-term plan?

The reality: Most homeowners who bought before 2023 still have substantial equity despite recent declines.

Refinancing May Not Make Sense

Lock-in effect works both ways.

Refinancing reality:

- Current rates around 6.5%

- If you have rate below 5%, don't refinance

- Breaking even takes years at higher rate

- Stay locked in to low rate

- Wait for rates to drop further

The advice: Don't give up a great rate for a mediocre one.

Home Equity Lines of Credit (HELOCs)

Access equity without refinancing.

HELOC advantages:

- Keep your low mortgage rate

- Access equity for improvements or needs

- Variable rates but flexible

- Only pay interest on what you use

- Don't reset your mortgage

The strategy: HELOCs let you tap equity without refinancing.

Market Predictions: What's Next

Where are home values heading?

Short-term (Next 3-6 months):

- Values likely to continue modest declines

- Depreciation may accelerate slightly

- Winter typically slow season

- Inventory continues growing

- Buyer leverage persists

Medium-term (Spring-Summer 2026):

- Market may stabilize

- Spring demand could slow declines

- Rates may drop slightly

- Prices likely to flatten

- Equilibrium emerging

Long-term (2026 and beyond):

- Gradual appreciation resumes

- 1-2% annual growth likely

- Market finds sustainable balance

- Affordability slowly improves

- Normal cycles return

The takeaway: Modest declines continue short-term, stabilization medium-term, gradual appreciation long-term.

Your Action Plan

Here's how to navigate this historic depreciation:

For Buyers:

- Recognize this as opportunity window

- Get fully pre-approved immediately

- Negotiate aggressively using market data

- Focus on long-term value, not timing bottom

- Act when right home appears

- Use experienced buyer's agent

For Sellers:

- Accept declining value reality

- Price aggressively below comps

- Make home irresistible with staging/repairs

- Be flexible on terms and timing

- Consider whether to wait or sell now

- Use experienced listing agent

For Homeowners:

- Don't panic about paper losses

- Understand your equity position

- Don't refinance out of low rate

- Consider HELOC for equity access

- Focus on long-term perspective

- Maintain and improve your property

Let's Navigate This Market Together

53% of homes losing value is historic, but it's not catastrophic. With Seattle down 2.5%, Washington down 0.98%, and the highest depreciation share in 13 years, smart strategy matters more than ever in Everett, Bothell, and Snohomish County.

As a Realtor specializing in market transitions and negotiation, I provide:

- Real-time market intelligence and pricing analysis

- Strategic guidance for buyers and sellers

- Honest assessment of your equity position

- Expert negotiation in declining market

- Protection and advocacy through closing

I'm available Monday through Friday, 8:00 am to 10:00 pm to discuss how this historic depreciation affects your specific situation.

Contact John L MerrellRealtor, Keller Williams EverettReal Estate Negotiation Expert (RENE)Cell: 425-480-6864

Let's turn this market shift into your opportunity! 🏡

John Merrell

| Merrell Properties LLC | Keller Williams Pacific Northwest | Keller William Realty Everett

or another way